29 Dec, 2023

The Seed Funding Struggle: How to Navigate Investor Pressure

In the dynamic world of startups, securing seed funding can be both an exhilarating and daunting journey. Not long ago,…

Digital wallets and real-time payments are becoming essential tools for small and medium-sized enterprises (SMEs) across Switzerland and Europe. As consumers increasingly shift to digital transactions, businesses must adopt these technologies to stay relevant, competitive, and efficient. This article explores the key benefits of digital wallets and real-time payments, and why SMEs should integrate these innovations to improve customer experiences, reduce costs, and enhance cash flow management.

A digital wallet, such as Apple Pay, Google Wallet, or TWINT (popular in Switzerland), stores payment information securely and allows users to make transactions via smartphones or other digital devices. These wallets simplify both in-store and online purchases, making them more convenient for customers.

RTP refers to the immediate transfer of funds from one account to another, providing businesses and customers with instant payment confirmations. Systems such as SEPA Instant Credit Transfer in Europe enable fast, 24/7 transactions, supporting seamless commerce.

Customers today expect seamless and fast payment options. Digital wallets eliminate the need for physical cash or card entry, providing a quick and frictionless payment experience. Real-time payments complement this by offering instant confirmation, boosting customer satisfaction.

Swiss Example: A small retail business in Zurich using TWINT allows customers to pay instantly via their smartphones, enhancing convenience and loyalty.

Real-time payments provide immediate access to funds, ensuring SMEs can manage working capital more effectively. Businesses no longer have to wait for settlement periods, which is particularly helpful during peak seasons or for time-sensitive operations.

Insight: Swiss SMEs participating in the SEPA Instant Payment scheme benefit from faster liquidity, enabling timely supplier payments and improved operational efficiency.

Digital wallets and RTP systems eliminate the need for expensive payment intermediaries, such as card networks, which can charge high fees. By leveraging direct account-to-account transfers, businesses can reduce operational expenses and improve margins.

Fact: A Geneva-based subscription business using SEPA Instant payments reports savings on transaction fees, compared to traditional credit card transactions.

Both digital wallets and RTP systems are equipped with robust security features. Digital wallets use tokenization and biometric authentication, while RTP integrates real-time fraud detection tools. These technologies reduce the risk of fraudulent transactions, providing peace of mind to both businesses and customers.

Compliance Benefit: Swiss SMEs remain compliant with European security standards, such as PSD2 and SCA (Strong Customer Authentication), by using these secure payment options.

By accepting digital wallets and RTP, SMEs can offer multiple payment methods to meet customer preferences. This flexibility helps attract a broader customer base, both locally and internationally, supporting business growth.

Example: An e-commerce business in Lausanne integrates Apple Pay, Google Pay, and SEPA Instant, making transactions smooth for both domestic and European customers.

While the benefits of digital wallets and RTP are substantial, SMEs may encounter challenges in adopting these technologies.

The adoption of digital wallets and real-time payments will continue to accelerate, driven by the growing demand for seamless digital transactions. As open banking gains traction, SMEs will have access to more innovative payment solutions, such as Request-to-Pay (RTP) services and embedded finance. Businesses that embrace these trends early will be better positioned to meet evolving customer expectations and stay competitive in a rapidly changing market.

Digital wallets and real-time payments are no longer optional—they are essential tools for SMEs aiming to improve operational efficiency, reduce costs, and enhance customer experiences. Adopting these payment solutions helps businesses build trust with customers, manage cash flow effectively, and unlock new growth opportunities.

For Swiss SMEs, staying ahead of payment technology trends ensures long-term sustainability in a dynamic market. Early adoption of digital wallets and RTP solutions will offer a competitive edge, preparing businesses for the future of commerce.

In the dynamic world of startups, securing seed funding can be both an exhilarating and daunting journey. Not long ago,…

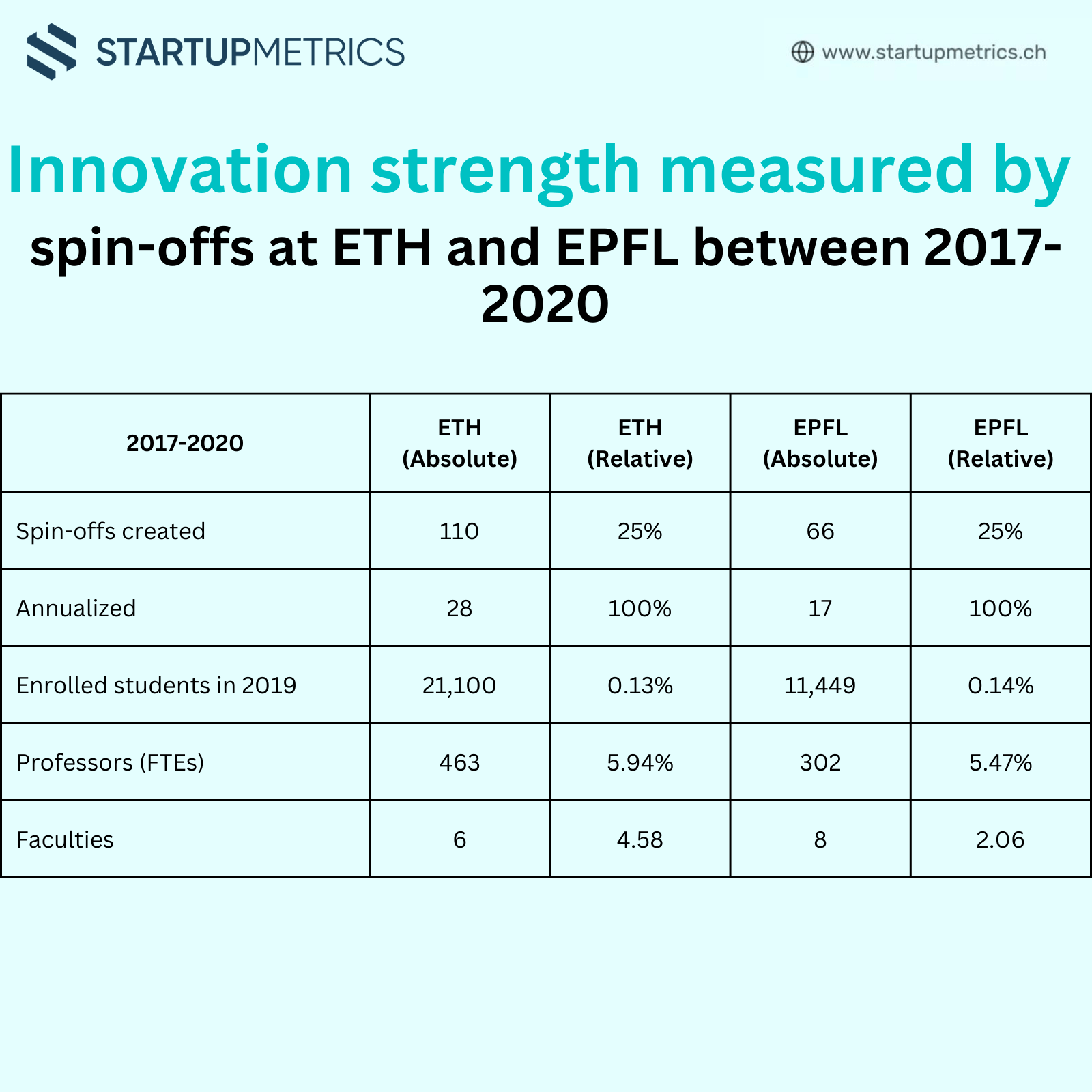

Members of the research institutions at ETH Zurich (ETH) and the École Polytechnique Fédérale de Lausanne (EPFL) launched 176 spin-offs…

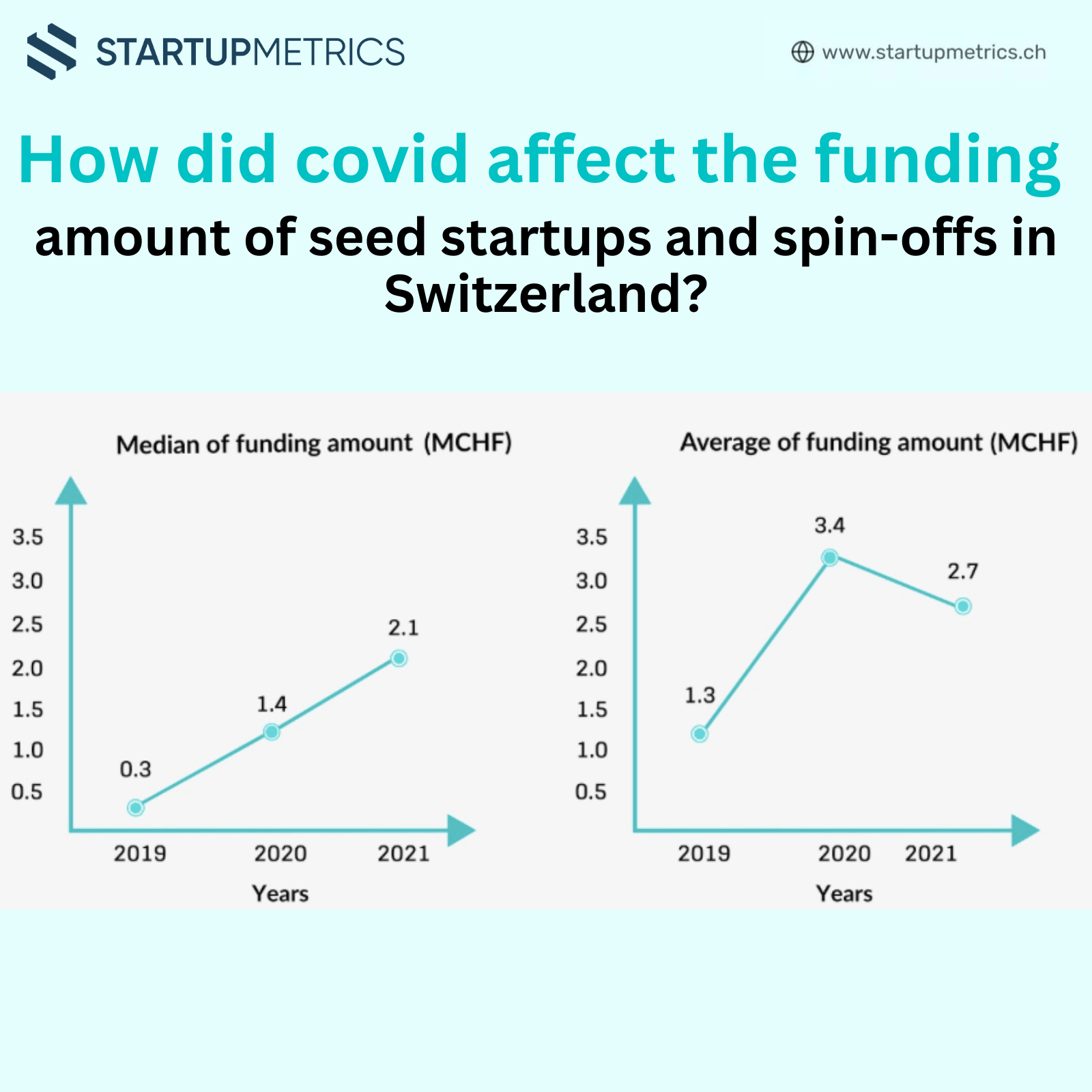

Positive Trends Amidst Challenges Overview Despite the global challenges posed by the COVID-19 pandemic, seed startups and spin-offs in Switzerland…

As a financial service, we work with many successful entrepreneurs. While working with each of them is very interesting, it…