15 Feb, 2023

The magic behind startup valuation in 2024

Determining the fair startup valuation is a critical and complex process. While many practitioners argue that startup valuation is more…

In an increasingly globalised economy, cross-border payments are vital for European SMEs expanding into new markets. However, these transactions come with challenges related to cost, compliance, and efficiency. With new technologies, evolving regulations, and emerging payment systems shaping the landscape, SMEs must stay ahead to thrive in 2024. This article covers everything European businesses need to know to navigate cross-border payments effectively.

The demand for real-time payments across borders is growing. New systems, such as SEPA Instant Credit Transfer And SWIFT gpi, enable faster settlements, giving SMEs instant access to funds.

Insight: In 2024, SMEs that adopt real-time cross-border payments can improve cash flow and enhance supplier relationships by avoiding payment delays.

SMEs are increasingly using multi-currency accounts to streamline cross-border transactions. These accounts allow businesses to hold multiple currencies and convert them at competitive rates, reducing the impact of fluctuating exchange rates.

Example: A Zurich-based SME exporting goods to Germany and France can hold both euros and Swiss francs, minimising conversion fees and exchange risks.

Blockchain-based payment networks, such as RippleNet, are gaining traction due to their speed and cost-effectiveness. Blockchain eliminates intermediaries, enabling SMEs to transfer funds across borders at lower fees and with greater transparency.

Open banking initiatives allow businesses to connect directly with financial institutions and payment gateways. SMEs can leverage open banking APIs for faster payment processing, automated currency conversion, and improved reconciliation.

Swiss Example: Open banking systems integrated with SEPA enable Swiss SMEs to transact efficiently with European clients.

Navigating regulations is a key challenge for SMEs. Cross-border payments must comply with local and international regulations, including PSD2 in the EU and AML (Anti-Money Laundering) requirements.

Tip: SMEs need to stay informed about KYC (Know Your Customer) policies and collaborate with payment providers who offer compliance support.

Cross-border payments often involve high fees, including conversion fees and intermediary bank charges. SMEs need to choose cost-effective payment providers or use multi-currency solutions to minimise these expenses.

Exchange rate volatility can impact profitability for SMEs. Businesses must adopt strategies like forward contracts or use hedging tools to protect themselves from currency risks.

Partnering with PSPs, such as Wise, Payoneer, or Adyen, helps SMEs reduce fees and ensure faster settlements. These platforms offer multi-currency accounts and competitive exchange rates.

Automation tools integrated with accounting software can streamline cross-border transactions, reducing errors and administrative burdens. Automated systems ensure accurate reconciliation and real-time payment tracking.

Example: A Geneva-based SME uses SAP’s automated payment system to monitor cross-border transactions efficiently.

SMEs must keep up with regulatory changes affecting international payments, especially with the rollout of MiCA regulations in Europe, which may impact cross-border crypto transactions.

In 2024, cross-border payments will become more seamless and transparent with advancements in AI-powered payment automation and blockchain technology. Emerging solutions like central bank digital currencies (CBDCs)will further streamline global payments, making them faster and more cost-effective.

Insight: Early adopters of new technologies, such as real-time payment networks and open banking, will gain a competitive edge in international markets.

For European SMEs, 2024 will bring exciting opportunities and challenges in cross-border payments. Businesses that embrace real-time payments, blockchain technology, and open banking solutions will thrive in the international market. Staying informed about regulations, managing currency risks, and partnering with reliable payment providers are essential for long-term success.

By adopting cost-effective strategies and automating payment processes, SMEs can streamline cross-border operations, reduce fees, and unlock new growth opportunities in a globalised economy.

Determining the fair startup valuation is a critical and complex process. While many practitioners argue that startup valuation is more…

As a financial service provider, we often encounter companies that offer exceptional products yet struggle with sales. This phenomenon is…

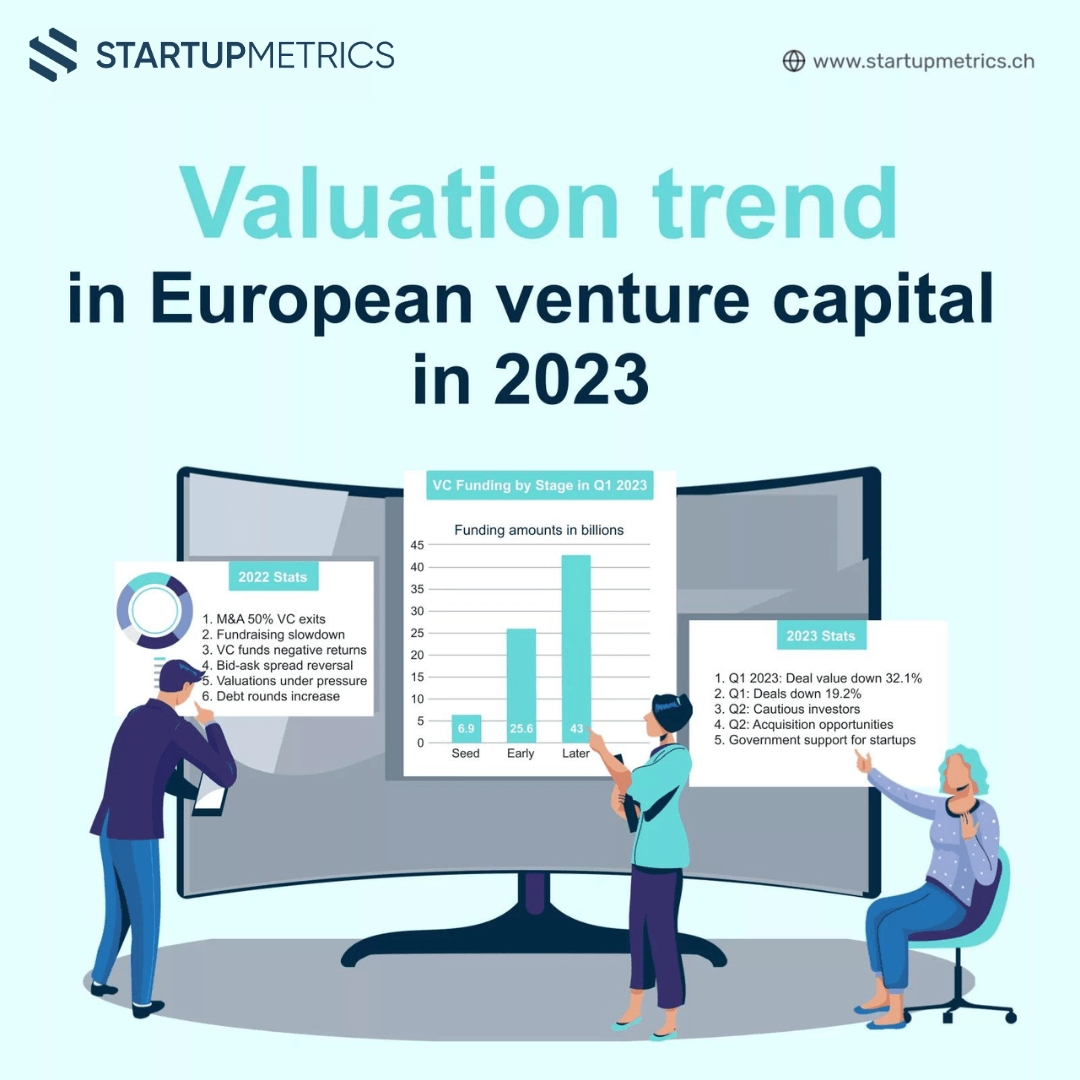

The European venture capital (VC) market is navigating significant challenges in 2024 as founders’ demand for funding continues to surpass…

Running a startup or business in Switzerland requires efficient financial management. To streamline your accounting processes and manage finances, it’s…